With just two days until the 2020 interim results announcement, now is a tricky time to make any predictions about the stock. With no COVID-19 guidance been given, a chain of acquisitions in March and April, and an aggressive selloff at the start of March, there are a lot of unknowns we have to make a best guess on.

You might not know the name Future Plc, the FTSE 250 listed firm, but you will know their brands.

What Does Future Do?

Future is a true multi-platform company. Magazines, websites, video content, and event live events. They are behind many of the brands you will recognise across technology, gaming & entertainment, music, creative & photography, home interest, education and television. Targetting both end consumers like us, as well as dedicated B2B industry offerings. Think a media company that loves technology.

Source: Future Our Business Model

Broadly speaking the company breaks down its business lines into two main segments. Media, which is their digital efforts and Magazine, which covers everything relating to print. A point to remember, media contains pretty much everything non-magazine for the ease of reporting.

Source: Future 2019 Full Year Results

The growing media efforts and B2B services now mean 54% of the revenue comes from the US, with the rest mostly coming from the UK. This means currency fluctuations will impact their earnings (strong dollar means weaker pound revenue.)

The reason I bring up technology earlier, the underlying platforms which powers many of their forums, sites, and advertising solutions is all inhouse managed and developed. This gives them the ability to scale their brands, and easily acquire and merge in competitors.

With their vast knowledge of managing successful brands, they also offer consultancy and other B2B support packages, but this is dwarfed by their advertising and e-commerce revenue streams.

Source: Future Investor Day 2020

One aspect which is interesting, and unique to digital content is the long tail of the pieces they produce and the affiliate deals they create.

Source: Future Investor Day 2020

Content created back in 2017 still attracts traffic and drive revenue even now. This creates a fantastic feedback loop with their digital channels.

A large part of the strategy is finding gaps in their offering, and acquiring competitors. Since April 2016 Future has completed over 10 acquisitions and spending over £171m. With a recent acquisition taking them in the video production and distribution space.

What About The Financials?

Traditional media has been under threat for some time, and an acquisition style of business can be expensive to maintain with the risk of expensive mistakes.

Source: Genuine Impact

You might be surprised at just how profitable Future is. However, you do need to look behind the numbers as they all tell a different story. A gross margin of 48% means they can bring in revenue at only half the cost. After the operating costs, this drops down to 13.6% operating profit which is a very impressive number to see. Finally, we look at the result and the final profit margin is a meek 3.7%. While they can generate a lot of revenue and covert that into profit, they are heavily reinvesting back into the business.

Additionally, this is a dividend-paying stock. The dividend is at the start of the year around January 16th, so we have completely missed it for this year. Don’t get too excited. The dividend yield is currently 0.11%, if you are looking to live off your investment dividends this won’t scratch that itch.

Source: Wallmine Future

The profit margin is consistent, they are a relatively low debt company considering their acquisition strategy, and they are easing their reliance on financing to support cash flow.

How Does The Value Looks?

After a nasty dip and some issues with short selling, Future is making a recovery back to the pre-COVID-19 dip.

Source: Yahoo Finance

We can see the price is struggling to keep any upward momentum and seems to have hit a ceiling recently. With the next update only two days away we are seeing the market protecting it’self from the unknown.

We haven’t had too much insight into the business over the last few months so confidence is knocked. That said, looking at the value metrics the company is priced about right.

Depending on your preferred ratios this is either overpriced compared to the price to book or extremely cheap versus book to share.

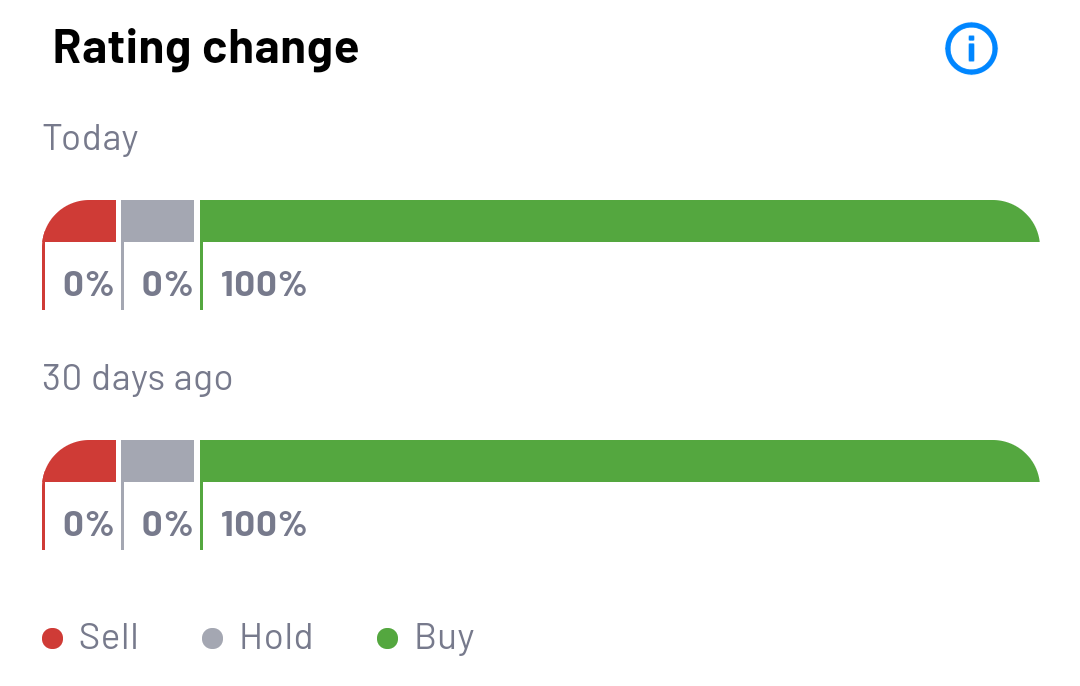

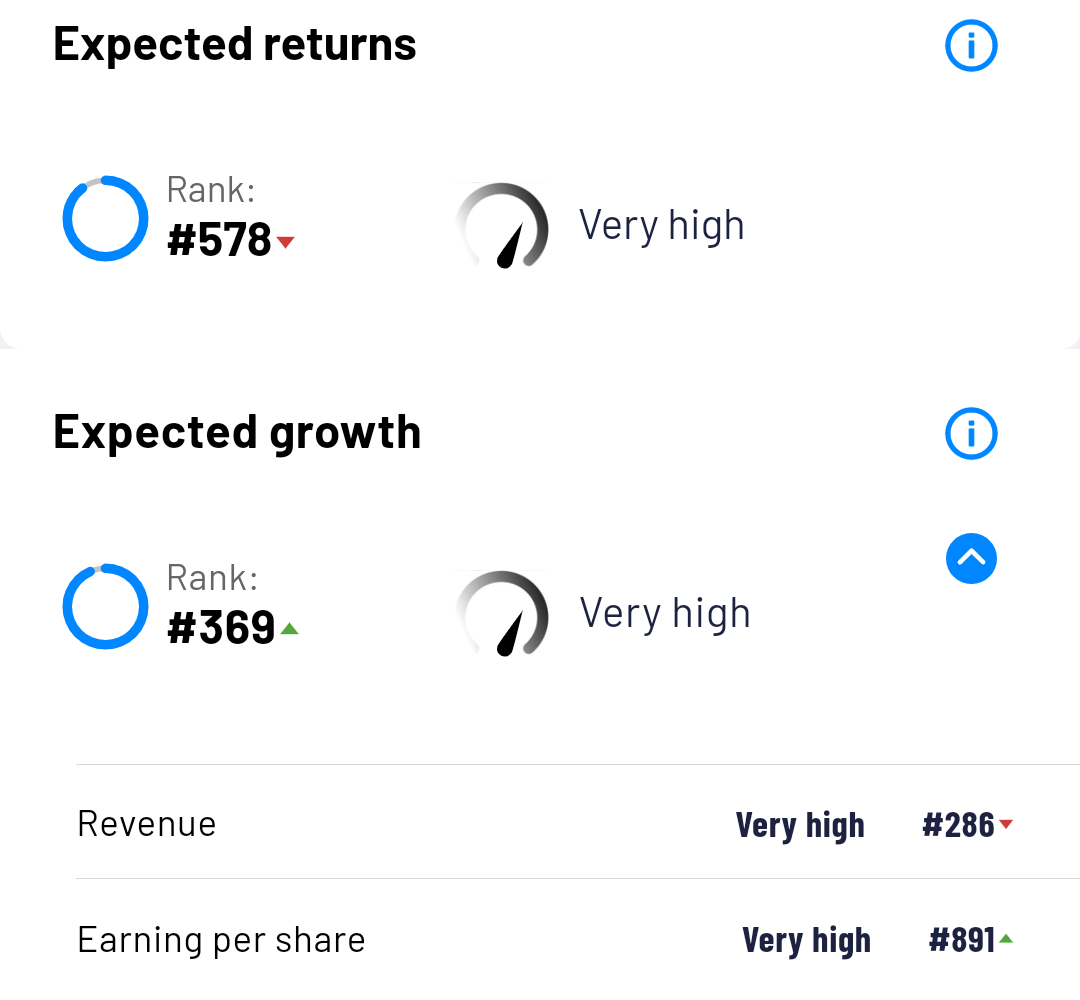

What Do The Sell-Side Analysts Think?

This is where analysing smaller companies can get tricky. I’ll spoil the punch line and let you know the analysts seem to love the future for Future. If you dig a little deeper, you’ll find only three or four analysts seem to be actively up to date and covering the stock, so we need to be a bit more careful with their views.

Source: Genuine Impact

The overwhelming buy rating is down to three analysts all having a buy prediction down. Depending on where you go for your data this number will be five to three. Three estimates seem to be up to date, and they are all buy’s but the target prices are very high.

Source: Genuine Impact

I had a deeper look into this and found two target price estimates both at 100%~ growth. While these feel like meaty estimates we can look at the numbers and try and backwards engineer what they are thinking.

If we look pre the price slash at the end of January after a short-seller attack, we were sitting at 1522p a share.

There was a month of recovery before COVID-19 changed the world as we know it. The analysts had set their original targets before the first dip, meaning the original change was 15-20% growth. As far as the business financials are concerned they have not changed.

Now COVID-19 has impacted the business, and we don’t know how badly. We know advertising budgets have been cut, at home spending has seen an increase, and online activity has jumped.

There is the potential that increased traffic has offset lower advertising budgets and potentially the lucrative affiliate e-commerce sales would have been boosted. Sadly with no new information, it’s pure speculation. We have to wait two days before we know for sure.

So Why A Buy?

I’ll admit, a buy rating this close to an announcement is more gambling talk than fundamentals. Even with an impacted business, this is still a cheaper business than it should be, we can see this looking back to the start of the year.

There is room for recovery and the market is padding in some extra protection against some unknown results. We could see a dip, like many, have experienced, where they have been hit by the economic slowdown. We know advertising is down and that is the main revenue driver. We also know activity is up for online forums and digital engagement, which Future also profits from.

It comes down to how much the advertising business has been affected. Events are off the table, TV and video production would have slowed, but online engagement should have skyrocketed. With no additional guidance, we are in the dark. I do think we’ll see the trading volume spike once some clarity (in either direction) is finally given.

Let’s hope it’s a return to their strong share price before, Back to The Future if you will.

I hope you enjoyed my write up and views. Please let me know what you thought, all feedback helps! Did I miss anything? Any aspects you wanted to be covered in more detail?

Thanks and stay safe.