Totally up to you.

I’m not running any bonds at all and have no intention either.

Stocks or ETF’s for me.

ETF’s for me does the same action as bonds, in regards to it lowers volatility and diversifies me a bit. There may be a place for bonds though, but I’m not going that route.

Completely subjective. But I would not go heavy into them, if I could offer that advice.

Imagine 2008- post crash, looking back which would you rather have more of : stocks or bonds going forward. For me stocks win.

I’m not too heavy into the bond but I do feel glad to have it unless post 2008 happens again but surely it won’t be the same as that was based off low offer mortgages which is ironic as the same year I got a 100% mortgage. Crazy times!

There could be a recession which I feel like I’m hunkering down for. Trying to figure out something safe I suppose and felt this bond was good for that.

I guess stocks weren’t hit that badly in 2008? I don’t know I was just a mortgage buyer back then.

Thank you. It’s always helpful to hear outside your own box

I think the crash was the worst of it, but I do expect another significant dip soon.

Either way though, it’s better put to work than sit in a bank at 0.05% return.

Don’t know if you’re joking or I’m misreading but in 2008 stocks had the biggest drops of all time. Basically created by giving out loans and

things like 100% mortgages without doing checks to see if they could afford or would ever get repaid.

It was a genuine question I think I spent the year purely fixated on the 100% mortgage we got and the fact I was offered an extra ££££ to do “additional work in the house” left in a daze. I can’t recall much more to be honest

In hindsight I do recall certain trade stores with a never ending sale on. I was in my own bubble then and definitely didn’t know or really comprehend the stock market back then.

I remember it of course but only for getting a mortgage deemed totally impossible today

@CeeGee One of the reasons for holding bonds as well as shares are that usually as assets they do not correlate with each other, hence adding some diversification of risk. So if shares fall then hopefully bonds will not fall as much or even rise; as you have found out with the Global Aggregate Bond.

So while holding Bonds can be seen as a way of diversifying risk especially for those who are “conservative” investors; such as people nearing retirement. Who do not want to deal with huge falls in shares as they will not have the time to wait for them to recover.

However they can also be seen as a source of cash to buy good companies and increase the number of shares in them. Which I think is what you are implying in your original post.

Therefore this could be a sound move depending on your goals, risk tolerance and time. So for example if your goal is retirement and you have a long time horizon ( 5 years + ) and you can tolerate that shares may go up and down in the short term, then it is a good idea to go with your strategy and top up on your favourite shares or ETFs.

The above is just an example and ultimately what you do will be based on your own personal circumstances.

Especially as all I have to go on is your username and icon. So I do not want to presume anything.

@Abel That’s make me smile. My logo is vintage - I sell vintage/up-cycled items but myself not quite vintage…yet

My goal is retirement with ETF’s, the Bond and various stocks (with “hopefully” 15+ years)

That’s great advice though, most definitely helped. I know the direction I’m heading sometimes I just want to make sure as a newbie that it makes sense to me and I’m making some head way and a sensible direction.

Every day is a learning day

Thanks once again for feedback, I keep it and refresh myself with it all often.

Dominance of the US stock market will fade. China on course to surpass US GDP in 2025. When the belt and road is up and running we will have a new world on our hands.

@Explorer2 here you go. It’s quite the epic read BUT it’s been absolutely incredible for my journey as a newbie I come back to this thread a lot.

I like you am thinking 10/15 years and so therefore am more able to take a risk but without reading into EVERY single stocks financial history for me covering the world with ETF’s felt the right move. Like I said I do hold single stocks and a few spec stocks (that’s because I love gold and mines in Aussie) I’ve made a few errors along the way but nothing that’s been too damaging it’s just helped me figure out my path.

Choose things you genuinely like and want to learn about.

Like I said dividends got cancelled early on so it made no sense me sticking with those companies because I wanted my free cash back for other things things I enjoy. Gold

Try not to overwhelm yourself (it’s so easy to do that in the beginning and even now to be honest) just take your time to read through.

I hope this thread helps as it sounds like you are thinking along the same sort of route as me.

You receive dividends from most of these ETF’s every quarter so that’s your dividend covered (yeah it’s not as big a % as some offer but least it’s not suspended) from there you compound that and invest more monthly (well that’s what I do)

It’s taken SO much stress off my shoulders too. Some say don’t pick all Vanguard and diversify but that’s personal preference personally I like vanguard I like their website and I like it all feeling together (except a few ETF’s which are medical/tech/property - they aren’t Vanguard)

Always with the questions - could someone please shed some light on something quickly.

I have WHEA (which isn’t fractional and I wish it was ) in my portfolio and it’s an accumulating fund.

Does that automatically go into the price - so I will see the price rise over time or is it displayed in the amount of shares I own?

I trust the system entirely so not worried about it just trying to figure out how or if I can see it for myself? Thank you I like that I don’t have to faff with dividends on an accumulating stock though.

I’m coming back to my old thread because the advice on here is second to none.

I don’t want to start a new thread and fill up air space with this question.

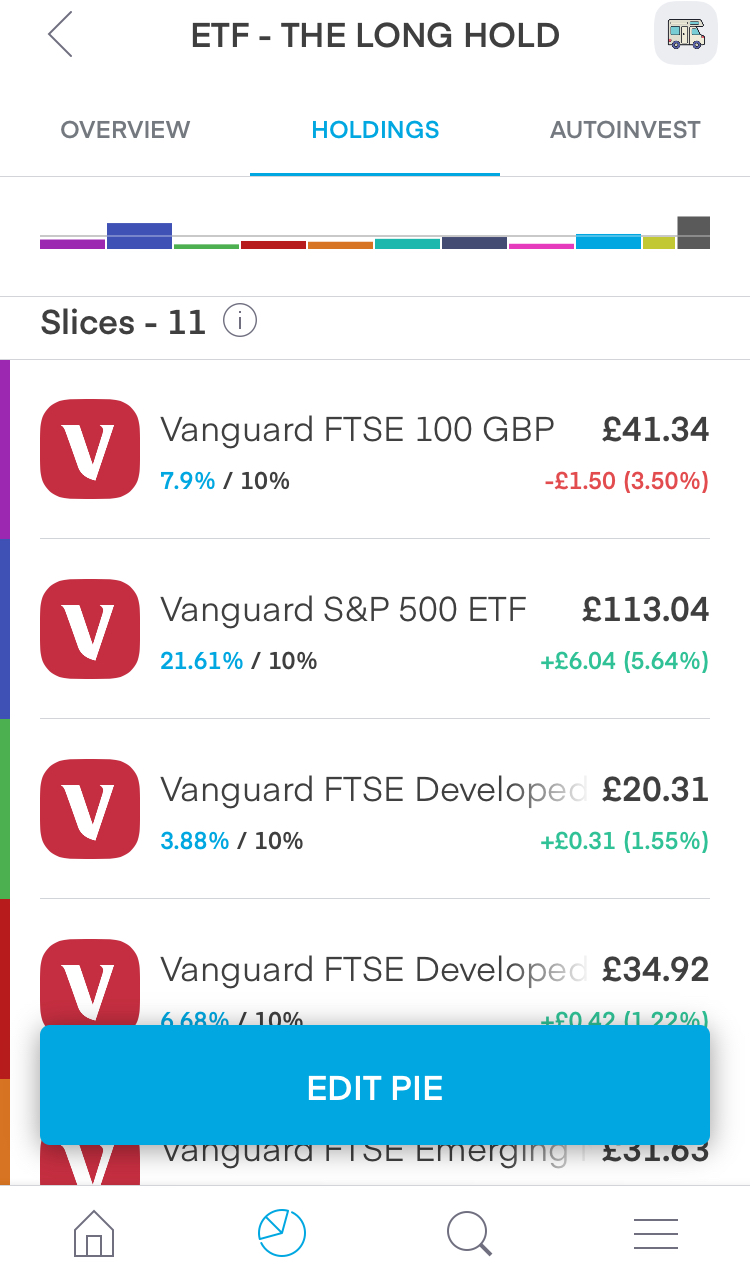

I’ve just been able to import all my ETF’s into PIE (fab now all snug in one place which makes me happy) when it comes to target weight and actual weight I’m a little confused.

I have 11 ETF’s that I want to invest in monthly but as I’ve been manually feeding them how do I decide how to set them into %

Do I set them by the actual weight on the left or make up my own on the right?

Hi @CeeGee, I think I answered you on another post regarding setting actual target weights.

In regards to your question about what % to set them too, the decision is in part related to your risk tolerance.

The screenshot shown has the target % of each pie/ETF which is 10%. In reality some slices are bigger (Vanguard S&P 500) and some smaller (Vanguard FTSE 100) due to the performance of the ETF.

Your decision is then whether to accept this or not.

If you are happy for some ETFs to have a bigger slice than others then you can leave it alone and adjust the target % weight to match the reality.

However if you think that it is too risky to have some slices bigger and others smaller and you want it all to be equal to 10%, then you can select the"rebalance" option.

What this does is that it will buy and sell the underlying ETFs so that you end up with the target % weights.

I’m sort of working it off the All World Vanguard ETF roughly. Perhaps I’m taking the slightly more risky approach with having a higher % in some than others. A few ETF’s like the MSCI and the wisdom tree cloud computing I just add what I can.

I think I’ve become so used to manually depositing monthly and working it out myself that I want to trust the auto invest to do it for me but worry I’ve set the % all wrong.

I’m still so new to it all. I guess as long as the yearly returns % reads + then I must have set something right?

It’s all becoming a little less clear as mud as I continue this journey

The good thing about your long term approach is you can try the auto invest function for 6 months, see the results, then decide if you want to continue with it or do it manually.

I think I spent the year purely fixated on the 100% mortgage we got and the fact I was offered an extra ££££ to do “additional work in the house” left in a daze. I can’t recall much more to be honest

I think I spent the year purely fixated on the 100% mortgage we got and the fact I was offered an extra ££££ to do “additional work in the house” left in a daze. I can’t recall much more to be honest

I come back to this thread a lot.

I come back to this thread a lot. ) in my portfolio and it’s an accumulating fund.

) in my portfolio and it’s an accumulating fund. I like that I don’t have to faff with dividends on an accumulating stock though.

I like that I don’t have to faff with dividends on an accumulating stock though.