Any thoughts that no directors have bought any further shares since the fund raise earlier this year?

Any ideas when the update will be if it not they met 2021 revenue projections?

I would have thought if they hit the 4m target they would be shouting from the rooftop as that would be a significant increase and potentially reduce their annual burn rate by up to 50%.

There have been quite a lot of partnership announcements recently and, to a lesser extent, earlier in the year, but I would assume that will contribute to next year’s revenue; not this year’s.

I don’t recall as many partnerships being announced last year (could be wrong).

Who knows, maybe they’ve blitzed the projections and that’s why they are quiet. But then, as you say, there might have been some buying. But wouldn’t that be insider trading?

I think we’re within our right to ask for a trading update to be honest, including management of cash flows. In fact I have asked if we can expect one similar to the timings between last years interim results and the 17th December update.

I might traipse back through their RNS’ of 2020, when I get some time, to see how many new partnerships they struck up. Using previous earnings as a guide, might be able to get a sense for where they are at.

Bidstack Group Plc (AIM: BIDS), the native in-game advertising group, is pleased to announce an agreement with a leading, global AAA game publisher. The multi-year and multiple advertising format deal will give the Company the ability to place advertising across the publisher’s mobile portfolio. The deal also gives Bidstack exclusivity to one of the world’s largest sporting franchises.

This significant partnership reinforces Bidstack’s global reach with inventory in key markets such as the US, the UK and EMEA. The genres are diversified across sports, life simulation, hyper-casual, racing, role-playing and open world and materially expands Bidstack’s addressable audience.

James Draper, CEO of Bidstack, said

“Closing this deal has been years in the making which, when fully integrated into every game, will add considerable reach to our network. Agreeing a multi-year deal with one of the most successful game franchises on the planet is testament to our product, technology and commercial teams’ work.”

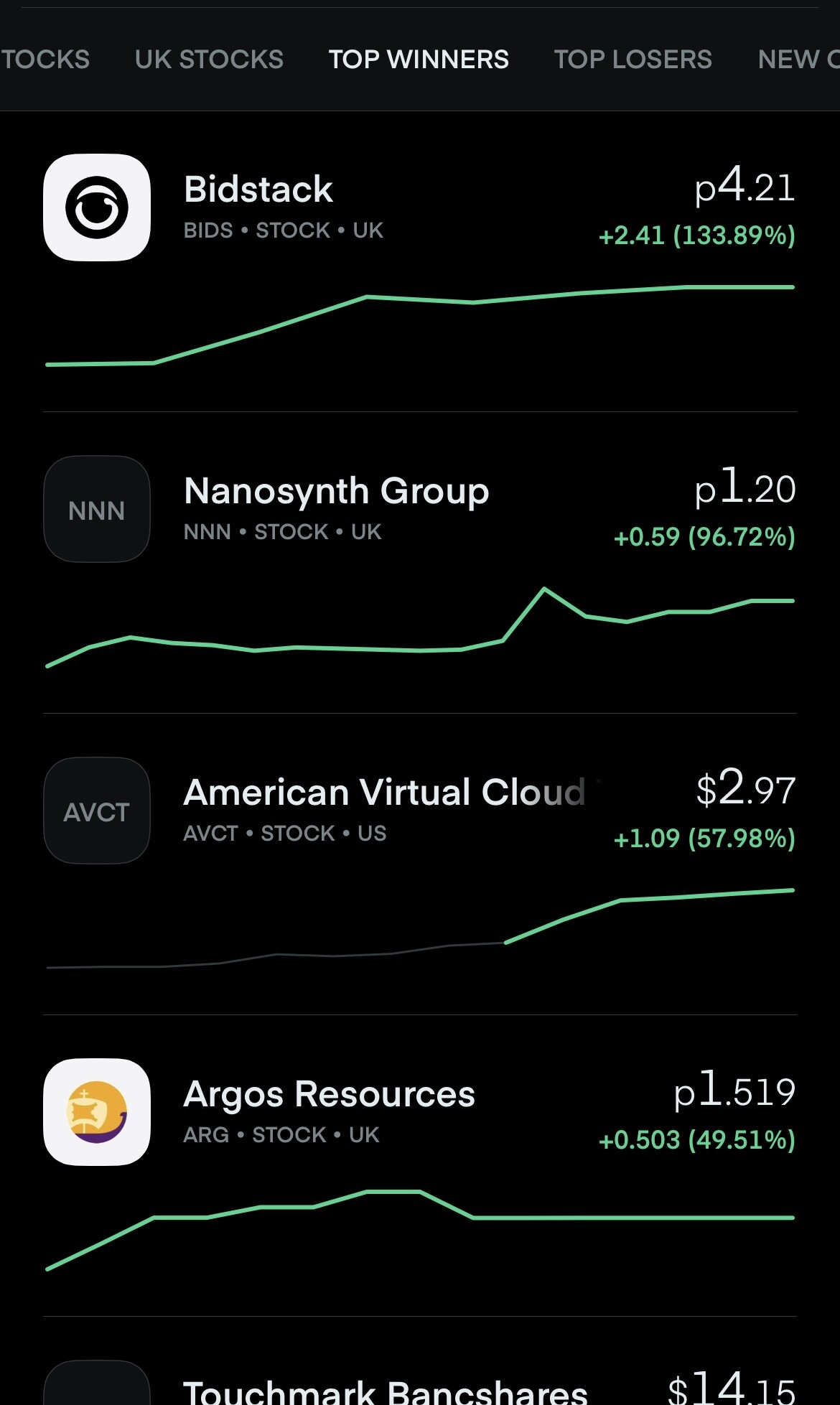

Funnily enough, I was going to buy a very small amount more today…(increase position slightly) and then I noticed that it had gone up a lot and searched for RNS. I won’t be buying today in the end, let’s see what happens first.

I already have a few shares, only a small amount considering it’s risk and limited information available.

Due to the recently signed commercial agreements, Bidstack has secured a revenue stream of a guaranteed minimum of US$30 million advertising spend over two years, commencing 1 March 2022;

As a result, and subject to audit, the Board expects FY21 gross margins to have improved significantly, to in excess of 30% (FY20: 13%)

I think this means BIDS will be profitable the next two years on the basis from this one deal they take a 30% cut…

In the short term I wouldn’t mind clarity on the 30% though and whether it’s 100% theirs, or divided between them, the gaming company and the advertising agencies.

On 2 July 2021 Bidstack completed an equity funding round with investors to issue a further 543.2m shares at 2p, raising a gross £10.9m before costs and leaving the balance sheet well capitalised. We estimate that this funding round will sufficiently finance the business through FY21E and FY22E based on current revenue forecasts and possibly through the profitability inflection point depending on the pace of revenue growth and gross margin achieved.

The Cenkos note is still well worth a read from earlier this year if not already. Hopefully they will update their analysis with the recent announcements.

I don’t think we will see another SP catalyst until February next year now, so continuing to hold. If/when it becomes reasonable to assume no further fundraising may be needed then we should see a further uptick.

In the ideal world, some of the directors should exercise their options to purchase additional shares at these current levels. This would provide an additional small cash buffer and boost confidence at current levels.

Trying to work out how the company is positioned in terms of future dilution risk.

Cash in bank 31 Dec

2021 7m

2020 2.35m

Revenue to 31 Dec

2022 8m estimate*

2021 3.5m estimate*

2020 1.7m

2019 140k

Also to note 10.86m raised through further fundraising round and another 1.1m from directors.

If we take the 2020 balance + fundraising less 2021 cash balance, then we get the 2021 cash burn of 7.3m.

Considering I estimate revenues to increase from 3.5m to 8m, the end of 2022 cash balance could be around the 4.5m mark.

In reality it’s squeaky bum time for Bidstack. They might just find themselves in a position where no more fundraising is required(except to help accelerate expansion). The actual 2021 results and company estimates should be the catalyst for any share price movement in 2022. The current share price I think is at the lower end of its fair value, but there are still so many unknown values it is difficult to estimate. This is likely why Cenkos have not adjusted their projected cash flows, nor target price for the company as things stand.

I have a small shareholding around 12,000 shares. I will consider topping up now if the price shows some weakness and falls back below the 3p mark in the near term.